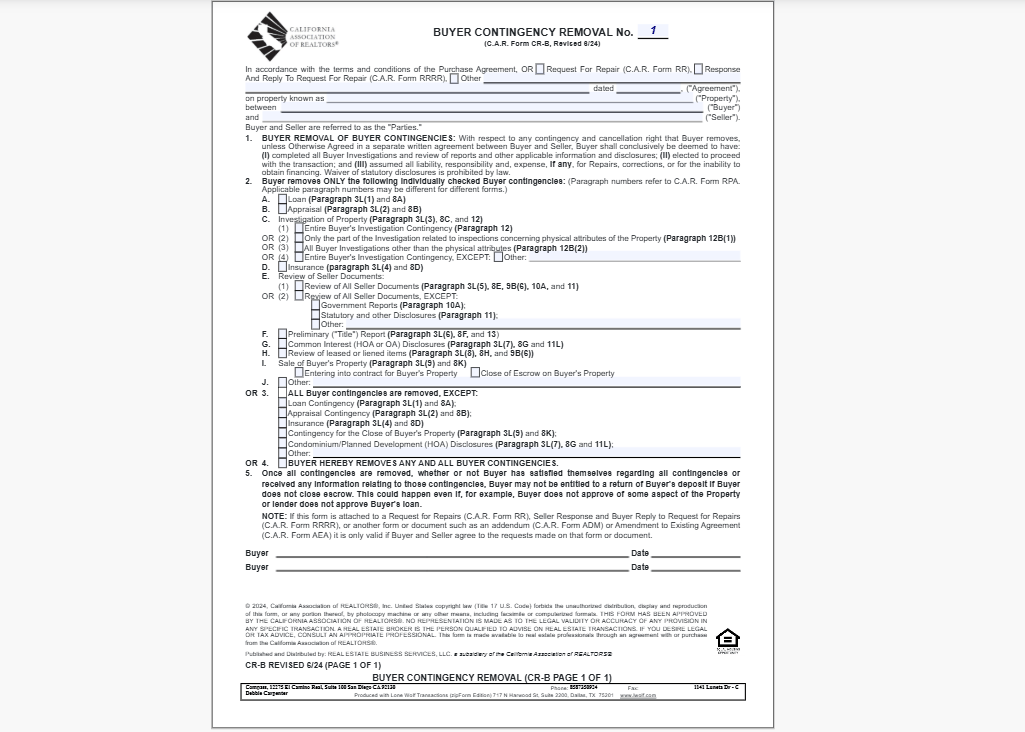

When a Seller accepts a purchase offer, they are committed to closing the sale — provided the Buyer fulfills their promises on time. The Buyer, however, has an important protection: the ability to back out of the sale if the right contingencies are in place. That's what makes the contingencies written into a purchase offer so critical, and having a great agent like myself can make the difference between success and failure.

Purchase offers typically include a refundable Earnest Money Deposit — customarily 3% of the purchase price here in San Diego. This deposit only "goes hard" (becomes non-refundable) after all contingencies have been removed by the Buyer. At that point, if the Buyer fails to close as promised — which is rare — the Seller may keep the deposit.

Selecting the right contingencies and carefully removing them during escrow requires skill and experience, which is why working with an agent like Debbie Carpenter makes such a difference. Here's an overview of the contingencies most commonly included in a purchase offer:

Property Condition — Typically includes inspections and often leads to a Request for Repairs, which opens an entirely new round of negotiation. Having a skilled agent in your corner at this stage is invaluable.

Seller Disclosures — All properties are sold "as is" and "as disclosed." This contingency covers the Transfer Disclosure Statement (describing the current condition of what's being sold) and the Seller Property Questionnaire (detailing the history of modifications and repairs).

Loan — Unless it's an all-cash offer, the Buyer must confirm they can secure the financing needed to close. Even a pre-qualified Buyer still needs the lender's underwriter to verify their application before a conditional approval is issued.

Appraisal — Required by the lender whenever there's a mortgage involved, and sometimes requested by the Buyer even in an all-cash transaction — particularly for unique or unusual properties.

Title — Verifies ownership and confirms who has the legal right to sell. It also clarifies what is included in the sale (such as a parking space), identifies any liens the Seller must clear before closing, establishes property boundaries, and discloses any easements that may affect the property.

Homeowners Association (HOA) — If the property belongs to an HOA, the Seller orders (and pays for) a package of HOA documents. These allow the Buyer to evaluate the association's financial health (including reserves), any pending litigation, board meeting minutes, community rules, and CC&Rs.

Insurance — The Buyer needs to confirm they can obtain adequate coverage at a reasonable cost — and that the policy meets the lender's requirements, if applicable.

Contingency of Sale — Sometimes a Buyer cannot close on their new home until their current home sells. Occasionally, a Seller will include their own contingency, making closing dependent on finding their next property. These situations can be complex, but with careful management by an experienced agent — like Debbie Carpenter — they can absolutely be navigated successfully.

If you have current questions, please give me a call – I love to talk real estate!